Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Retirees who have worked hard and saved carefully may consider buying a larger home better suited to pursuing new hobbies, small business ventures, or hosting family gatherings. For those who have accumulated many belongings over the years or are storing the possessions of college-aged children who haven’t yet settled down, a larger home allows for greater storage.

As a move can be stressful, give yourself plenty of time. You should draw up a moving checklist so you know in advance everything you’ll need to accomplish to get from A to Z. Include precautions to avoid injuring yourself with heavy lifting, especially if you have a lot to transport. If you have family members who are considering residing in your new home, ask them for assistance in moving. You could also hire a senior move manager to assist in relocation.

If you are hoping to move into a larger property, important considerations include financial preparation, knowing the specifications you’re looking for, and of course location.

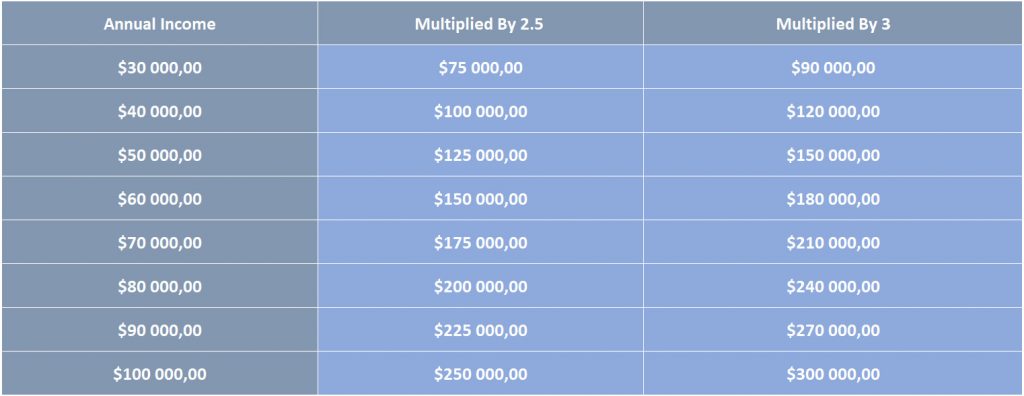

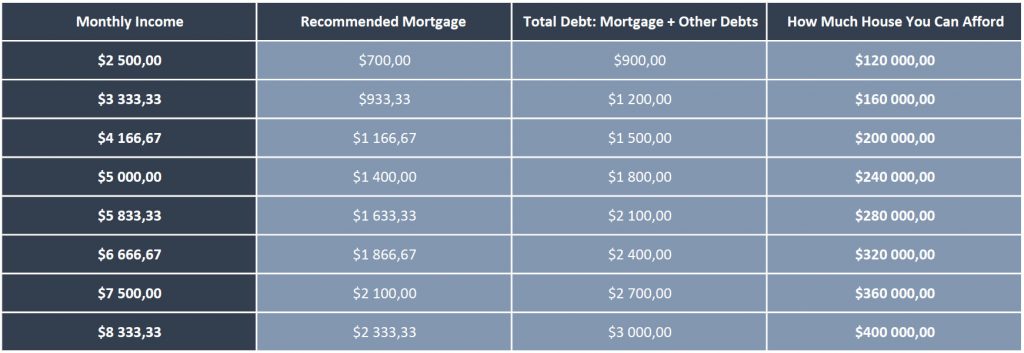

Debt elimination will increase buying power.

The key to financial preparation is dealing with debt. While it’s not unusual to carry debt into retirement, your buying power is significantly hampered if you owe a lot on credit cards, outstanding medical bills, or other loans. Try to budget a few years in advance of retirement to pay off as much as possible. Research debt consolidation plans to see if any might work for you. And watch your , as your ability to get a good rate depends largely on this.

If your debt is large, try contacting a credit counseling agency and working with a certified debt relief specialist, who can help you find a debt management plan that is right for you, depending on how much you owe, your ability to pay it back, and your regular income.

Figure out what to do with your existing property.

If you are approaching retirement with an existing mortgage, you probably need to sell your existing property and pay off the remaining debt to have funds for a down payment. Another option might be using your smaller home as a rental to generate income to finance your new purchase.

If you intend to use the proceeds of a house sale to purchase a larger property, find out how much you are likely to get – and how quickly. Make a contingency plan in case you need an interim place to stay, between selling one home and acquiring another.

Be clear on what you are looking for in a new home.

Research considerations such as zoning, laws affecting small businesses, and any restrictions on the use of land for farming or livestock. Also, know how much acreage you will need if you intend to keep farm animals, what type of land is ideal for flower or vegetable gardens, and whether additional water sources or drainage will be needed.

When considering different homes, take notes on what you’re looking for in terms of square footage and the number of rooms. If you plan to use your house as a craft shop, small business, or bed-and-breakfast, educate yourself on any regulations regarding occupancy, wiring, food safety, and plumbing. Will you need another kitchen? Extra bathrooms? An attached outbuilding? Research what modifications might cost, too.

Location matters.

While real estate will certainly be cheaper in remote or less upscale areas, such areas may lack the population or infrastructure to make your dreams a reality. If you are planning on opening an online shop, or are interested only in gardening as a hobby, a remote location might not be a drawback. But if you hope to draw customers into your home, you will want to be adjacent to a more populous and thriving region. Also consider proximity to grocery stores and hospitals, and whether roads will remain passable in severe weather.

You have worked hard to earn your retirement. It’s important that you be able to enjoy it as much as possible. With careful planning, you can look forward to many active and rewarding years in a new and larger home.

When you’re ready to begin your search for a new property in retirement, get in touch with Realtor Paul Burrowes by visiting the website or calling (831) 295-5130.

Image via

Image via